Midway through a build, materials arrive at a higher price than the estimate. No one flags it, so the job keeps moving.

A few weeks later, someone approves a change on site, but it never makes it back into the estimate. A few small items get handled “later” and never reconciled.

At closeout, the margin comes in lighter than expected. Nothing blew up on site, so the job ran smoothly. But the numbers stopped matching.

Most builders think cost control is about monitoring spend during the build: reviewing invoices, checking reports, and comparing actuals to the budget.

But by the time you’re monitoring, the drift has already happened. Cost control problems rarely show up as obvious mistakes. They show up when, after you win the job, the estimate stops acting as the source of truth.

This guide explains what cost control in construction actually depends on, what happens to it after you win the job, and how to identify the moment the numbers stop carrying forward before the profit is gone.

What Is Cost Control in Construction?

Cost control in construction is the process of comparing what you estimated to what you actually spend and catching the difference before it eats your margin.

In practice, that looks like pulling up bills after a delivery to see if lumber came in at the price you bid, checking subcontractor bills against the line items in your estimate, and running a job cost report near closeout to figure out where the money went.

Most builders treat it as a financial review, something that happens after the spending decisions are already made.

That framing assumes the estimate you created still reflects reality by the time you compare it to actual costs. These assumptions include:

- The prices you pulled are still the prices you are paying.

- The quantities you measured still match what you’re building.

- The allowances you set still cover the selections you’re making.

In most jobs, those assumptions protect the margin, but when one breaks, the job absorbs the difference.

The Cost Control Process in Construction Projects

Cost control follows a sequence most builders already work within, whether or not they’ve formalized it.

It starts with the estimate: quantities, material costs, labor hours, subcontractor pricing, and allowances. This is the financial baseline that defines what the job should cost before any work begins.

Once accepted, the estimate becomes the project budget. That budget assigns spending limits across cost categories: framing, electrical, plumbing, finishes, and site work. Each category has a number that represents how much the job can absorb while still protecting margin.

Purchasing translates those numbers into commitments: dealer orders, subcontractor agreements, and material deliveries.

During execution, you record the actual costs you incur. Dealers send invoices, subcontractors bill for completed stages, crews log labor hours, and teams collect receipts for incidental purchases. Each entry converts what you planned into what you spent and tests whether the original numbers still hold.

Reconciliation compares those actual costs to the budget, category by category. Review at closeout measures total actuals against the original estimate to assess performance.

The logic is straightforward: set expectations upfront, translate them into commitments, track spending as work progresses, and catch deviations early enough to respond.

But the loop only holds if the numbers survive each handoff intact. If purchasing, change orders, and invoice entry drift away from the original estimate—even slightly—the control process becomes reactive rather than preventive.

Why Cost Control Breaks Before Closeout (and Where It Breaks)

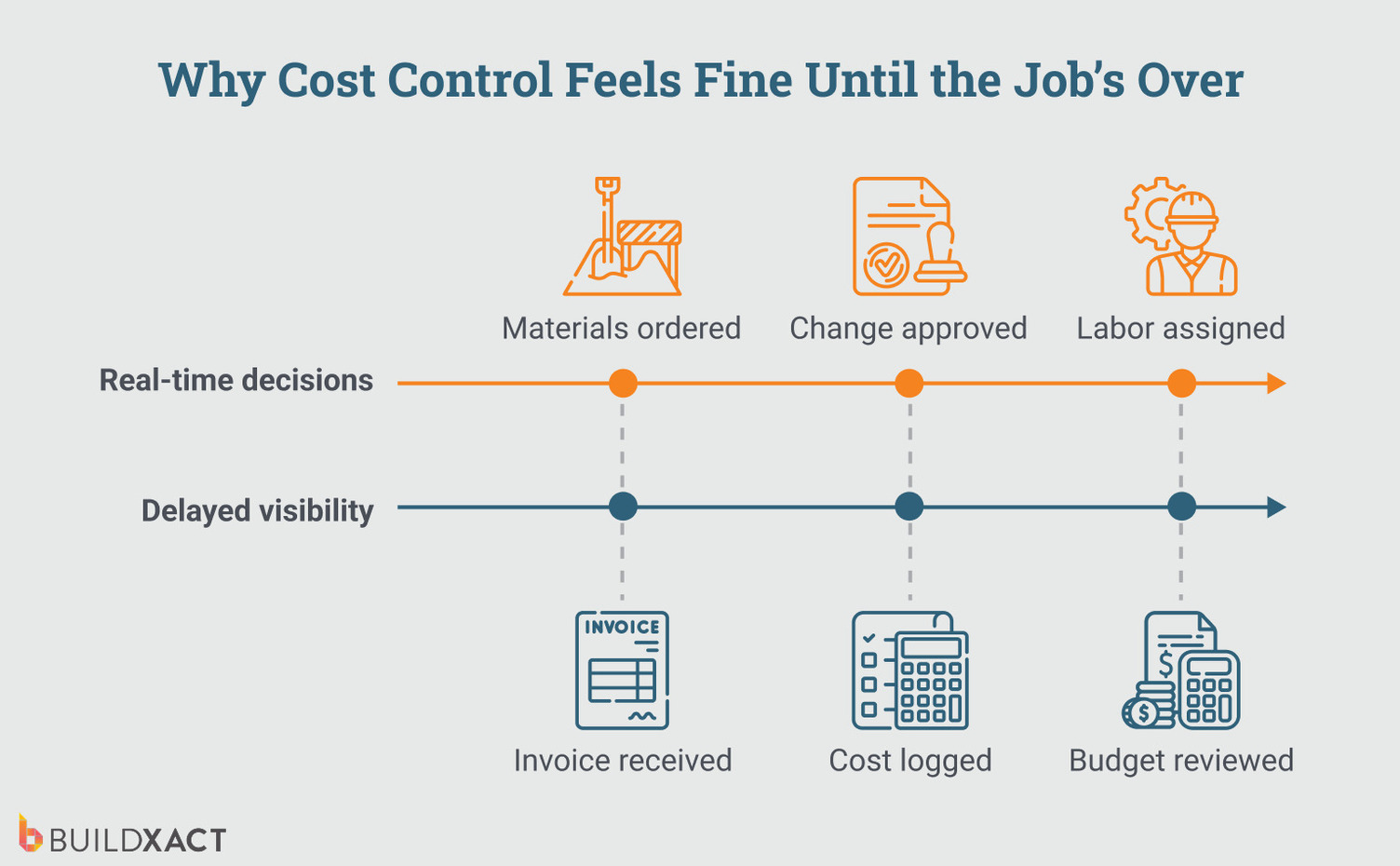

Cost control often appears to be working because you make spending decisions before you see their financial impact. You order materials, schedule subcontractors, and approve change orders as the job progresses.

You compare those costs to the budget only after invoices arrive or reports run. By the time you see the variance, the commitment has already been made.

That timing gap is where the margin disappears through a series of reasonable decisions that felt justified at the time.

According to NAHB’s 2025 Cost of Doing Business Study, the average single-family builder operates on an 8.7% net profit margin.

That’s the highest it has been in three decades, and that means there’s almost no buffer between a job that made money and one that didn’t.

A few untracked price increases, a couple of unpriced change orders, and that margin is gone.

Where cost control breaks

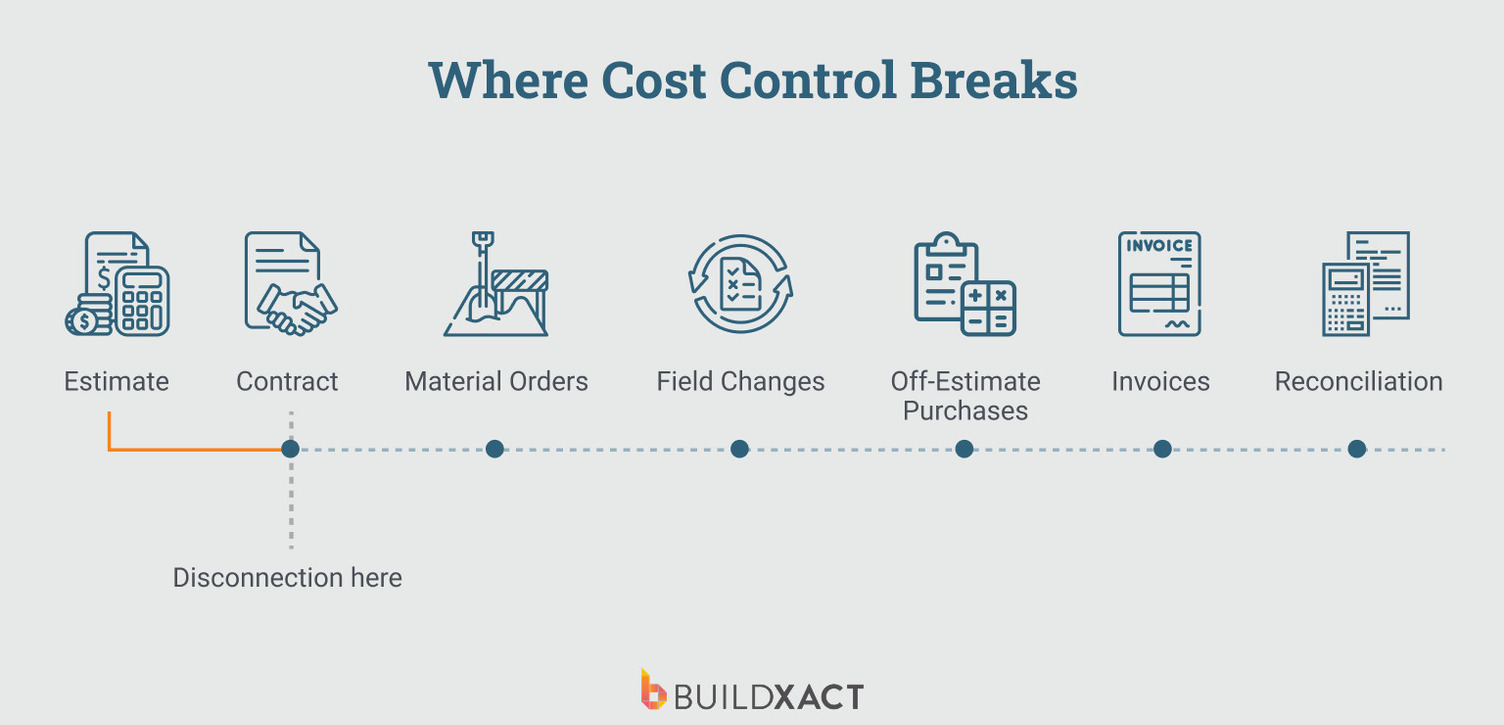

You can trace the breakdown of cost control to a handful of predictable decision points.

Ordering materials without checking current prices

A builder puts together an estimate, wins the job, and orders materials weeks or months later using the prices from the original takeoff. Between the estimate and the purchase order, lumber moves, hardware pricing shifts, and dealers adjust rates.

Tariffs and supply volatility have pushed construction material costs up by an estimated 9% in recent market projections, according to Cushman & Wakefield. That kind of movement does not need to be dramatic to affect a job’s margin. It only needs to happen between the day you submitted the bid and the day you place the order.

When the order goes through at a price the estimate did not account for, the dealer invoice replaces the estimate as the governing number. The estimate no longer sets the cost. The invoice does. From that point forward, the variance becomes permanent.

Letting work proceed before pricing the change

A client asks for a change on-site. You agree because stopping the job to price it feels more disruptive than moving forward. The plan is to calculate the cost later, update the estimate afterward, and complete the paperwork once the schedule allows.

But your busy schedule rarely allows it. Crews complete the work, materials are installed, and the job incurs costs before anyone revises the numbers. What started as a temporary shortcut becomes a committed expense.

Steve Griffin, estimator at Just Building Group, described how easily change orders slip when systems fragment: “In the old days, paper and pen, emails, plans if there is a change in office, it’s left on someone’s desk, gets put under a pile of other paper, and the change order doesn’t get to the supervisor, doesn’t get to the dealer.”

That breakdown is about control. Once labor and materials are committed, the estimate no longer governs the cost. The job carries the expense whether or not it was priced. At that point, the builder is no longer deciding what the change should cost. The builder is deciding how much margin to absorb.

Absorbing “small” purchases outside the estimate

Small purchases rarely trigger a pricing review. A box of screws here, a tube of adhesive there, an extra trip to the dealer to grab something the crew needs to finish the day. None of these expenses feels large enough to warrant reopening the estimate or pausing the schedule.

Since they bypass the original line items, they never pass back through the pricing structure that defined the job’s margin.

Each cost looks insignificant individually, but collectively they shift the job away from the numbers you bid.

Small, untracked costs accumulate outside the estimate. Over the course of a job, they erode the margin. Across multiple jobs, they distort your understanding of what your work actually costs.

Paying invoices and logging costs without revisiting the estimate

Cost control weakens when you process payments without checking them against the estimate.

Dealers deliver materials and send an invoice. A subcontractor submits a progress claim, and a team member makes an in-store purchase for items needed that day.

Those invoices need to be paid. Dealers expect payment on agreed terms while subcontractors expect timely processing. So the priority becomes keeping accounts current and jobs moving.

In that moment, accounting becomes the reference point instead of the estimate. The job absorbs the expense, but the line item in the bid does not get revisited. So the cost is attached to the project total without being tested against the planned amount.

When you compare final job costs to the estimate, the commitments have already been made.

The overrun does not appear suddenly; it reveals that the estimate stopped guiding decisions earlier in the build.

The financial disconnect becomes visible only at closeout, when you compare total job costs to the original estimate and realize the estimate stopped governing decisions earlier in the build.

How the Estimate Keeps Cost Control Working After You Win the Job

Cost control fails the moment the estimate becomes a reference document instead of a governing system. When that connection stays intact, here’s how the pattern reverses:

The estimate stays active after you win the job

In disconnected workflows, builders re-enter material lists into dealer portals, check pricing separately, and recreate orders outside the estimate. That step creates drift.

When purchasing pulls directly from the estimate, the same line items, quantities, and cost structure carry forward into the order. Live pricing and store-specific discounts apply at checkout, so the price you see reflects what you will actually pay.

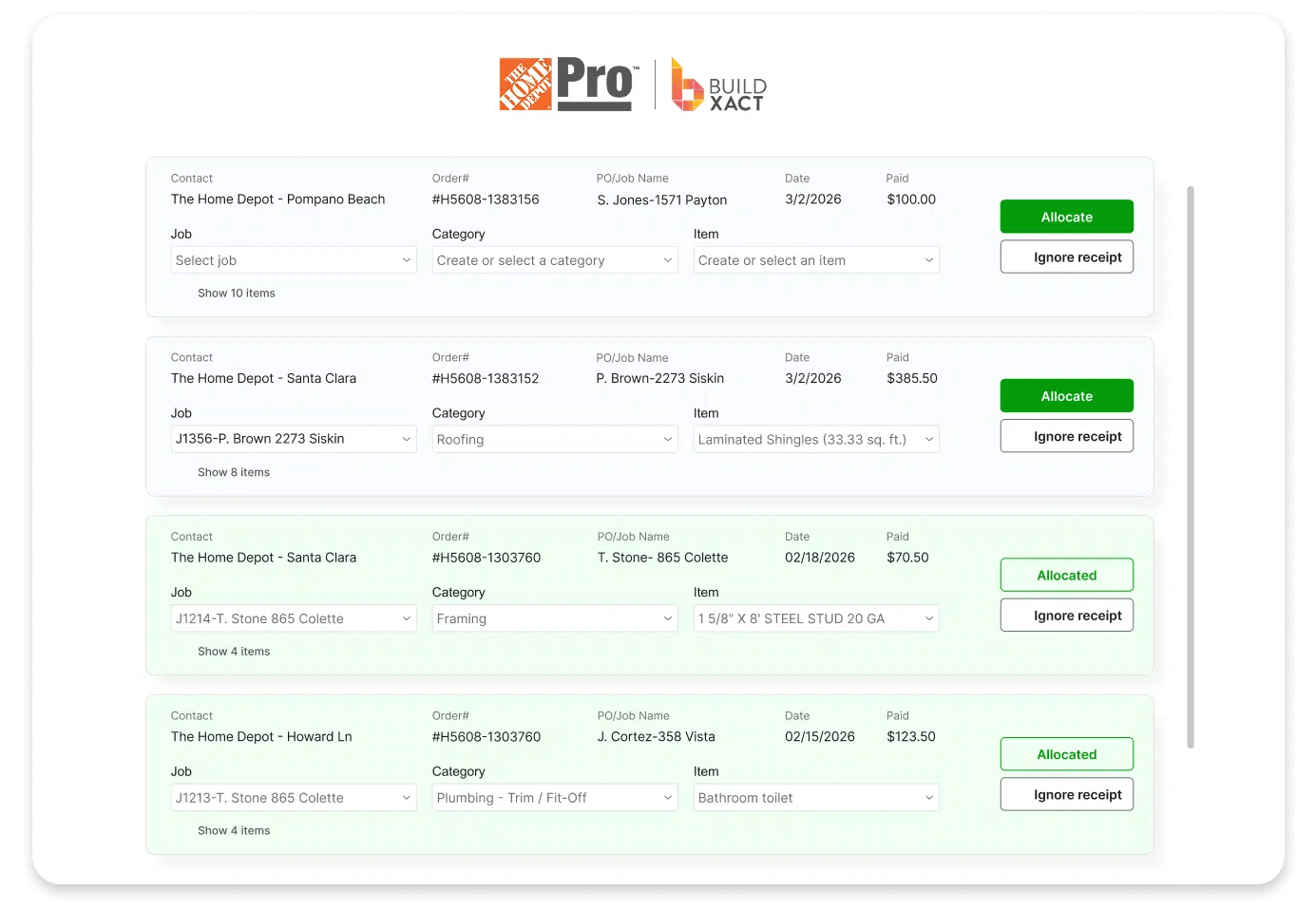

With Buildxact’s direct ordering connection to The Home Depot, you can now generate material orders from your estimates, view current Pro Xtra pricing, and have receipts automatically sync back into the job.

That keeps the budget, the order, and the actual cost aligned without manual re-entry.

As Joshua Bradley, a custom home builder using Buildxact’s integration with The Home Depot, describes it: “You click it, and in a couple seconds, it’ll load, and it will populate whatever’s in that estimate with the latest Home Depot price, and it will lock it into that price.”

That shift does not stop price movement in the market. It ensures the estimate reflects current pricing before the order leaves the job.

Change orders stay tied to the original numbers

When you capture a scope change inside the same structure as the original estimate, the pricing stays anchored to the job’s budget. You update the same line items, adjust quantities or labor hours, and generate a revised total before work proceeds.

For example, if a client upgrades from laminate to hardwood, you do not approve the change; sort out the pricing later. You revise the flooring line item, adjust material quantities, update labor time, and issue a change order that reflects the new total before installation begins. The original allowance and the revised cost remain visible in the same budget category.

If a framing detail changes and requires additional lumber and labor, you update the framing category before the crew commits to the work. The estimate reflects the new cost structure immediately, and the job total adjusts before materials leave the yard.

Nothing waits until closeout to reconcile. The budget updates when the decision changes because the change moves through the same pricing structure that defines the job’s margin, so that it cannot be accumulated outside the estimate.

This is where small scope adjustments stop compounding into losses that only become visible after the project finishes.

Paying invoices without reviewing against the estimate

Cost control breaks when invoices are entered into accounting without being reconciled to the original estimate. The job absorbs the expense, but no one checks whether it matches the bid.

With Buildxact, receipts from The Home Depot sync directly into the job. Before they affect totals, they must be assigned to a project and cost category. Builders can also allocate them to the exact estimate line item to which the purchase relates.

If a lumber order was estimated at a certain amount, the receipt is attached to the same framing line. The system shows immediately whether the actual cost aligns with the bid amount. If it does not, the variance appears inside the category that controls the job’s margin.

That shift changes timing. The comparison occurs when the cost is entered into the job, not during a reconciliation meeting weeks later. Margin movement becomes visible when money is committed.

Margin becomes something you can see, not guess

When quantities, pricing, change orders, purchasing, and receipts remain tied to the original estimate structure, margin stops being something you calculate at the end of the job. It becomes visible inside the workflow that produces the cost.

Each category shows what you bid and what has been committed. Each purchase and change orders update the same financial structure that defined profitability at contract signing. There is no separate reconciliation spreadsheet, and no reconstruction is required at closeout.

When the estimate carries forward through purchasing and actuals, profit does not rely on post-job analysis. It reflects the decisions being made during the build.

Keep Costs in Check with a Connected Workflow

Cost control depends on whether the estimate continues to govern decisions after the job is won.

When purchasing, change orders, and receipts move through the same structure as the original estimate, the budget updates as decisions change. Change orders appear inside the categories that define margin, not weeks later in a report.

Buildxact connects estimating, ordering, and job costing so the numbers that win the job remain the numbers that guide it.

Instead of reconstructing performance at closeout, you see how each commitment affects the estimate as the job unfolds and adjust before small gaps turn into permanent losses.

Start for free or book a demo and see your estimate carry forward into purchasing and job costs so margin becomes something you control, not something you discover after the job is done.